")

Blood bath on Dalal Street, foreign investors’ exodus, mass selloff, several lakh crore of investors’ wealth wiped out – these are the headlines that have dominated financial news this month. The US-Israel-Iran war has dealt a massive blow to the Indian stock market indices BSE Sensex and Nifty50 which were already struggling for the last few months after Donald Trump announced tariffs.With global crude oil prices rising to levels not seen in several years, the inflationary impact globally and its resultant blow to GDP growth has kept investors on tenterhooks forcing them to flee riskier assets like equities.The selloff by foreign institutional investors (FIIs) has been particularly pronounced. Rupee has seen its worst financial year in over 14 years, breaching the 95 per dollar mark in trade on the last trading day (March 30) of the fiscal year.At the start of the new financial year 2026-27, what’s the outlook for BSE Sensex and Nifty50? When will foreign investors become net investors?

Sensex & Nifty Round-Up – Facts & Figures: A Telling Picture

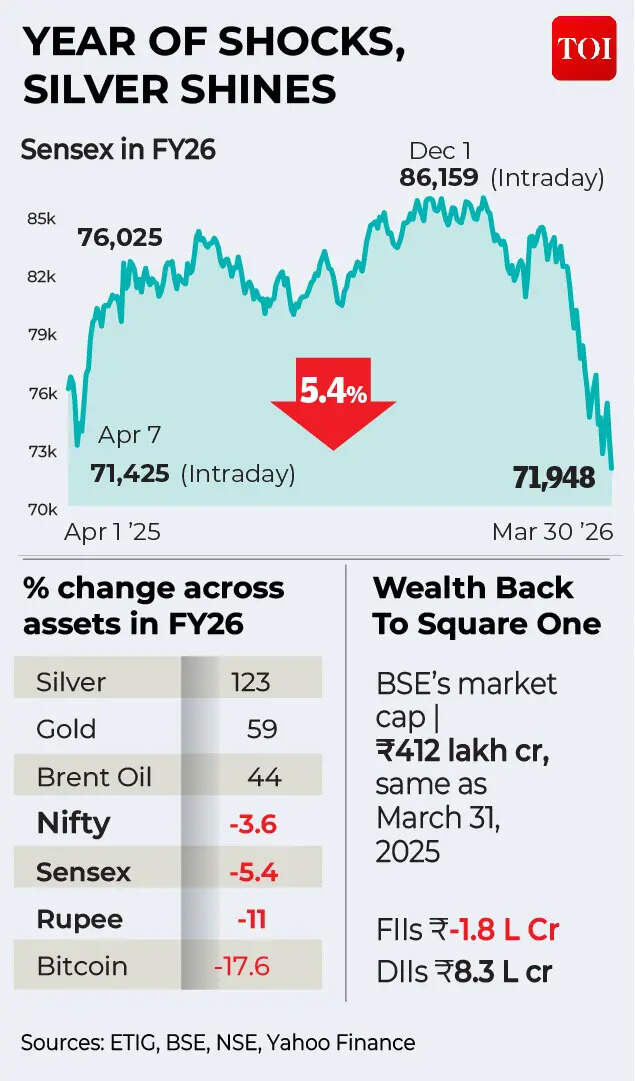

- From the start of the Middle East conflict on February 28 (Saturday), investors have lost Rs 51.7 lakh crore so far! The market capitalisation of BSE-listed companies has come down to Rs 4,12,41,172.45 crore (March 30 closing) from Rs 46,325,200.41 crore (February 27 closing). The current market cap stands at $4.3 trillion.

- In a span of just a month, BSE Sensex is down over 9,300 points or 11.48%! Sensex is actually down almost 16.5% from its all-time high level of 86,159.02.

- It’s been a bad month for foreign investors’ exodus, with over Rs 1 lakh crore (around $12 billion) withdrawn from domestic equity markets in March. This is the worst monthly outlook in Indian stocks.

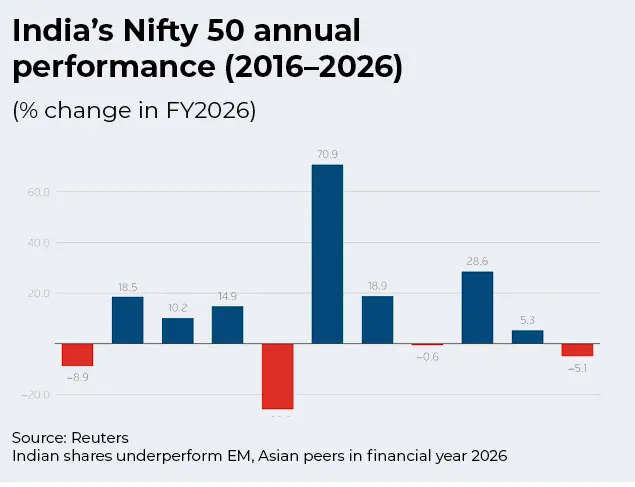

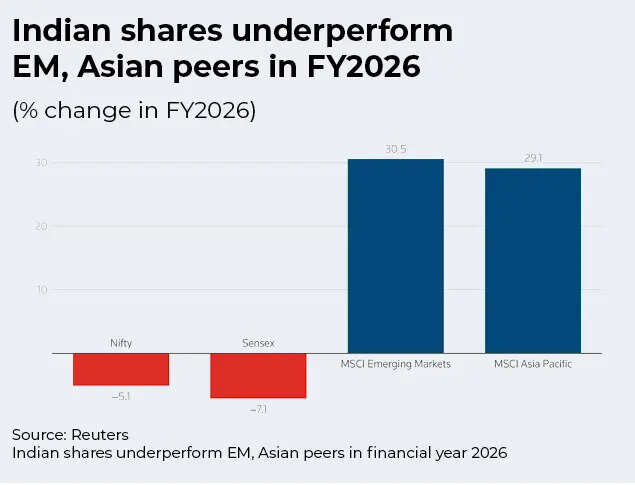

- In the financial year 2025-26, Sensex dropped 7%, ending on a bearish note with no clear horizon on when an uptrend will begin. Nifty50 has dropped 5% in the same fiscal year.

- In fact, the market cap of BSE-listed firms has not budged in the last year. According to a TOI analysis, BSE’s market capitalization at Rs 412 lakh crore is exactly the same as it was on March 31, 2025!

- Not only that, the March 2026 closing is even below the closing for March 2024! On March 28, 2024, Sensex closed at 73,651.35. At present, Sensex is at 71,947.55, down 1,700 points from two years ago!

- In FY26, foreign funds took money out of Indian stocks at a record pace. The total net outflow stands at Rs 1.8 lakh crore, which is the biggest annual outflow.

- Domestic players continue to cushion the stock market fall. In FY26, domestic institutional investors bought stocks of around Rs 8.3 lakh crore.

Analysts are of the view that the risk aversion seen in stock markets in March is one of the worst since the Covid pandemic back in 2020.

Why are foreign institutional investors rushing out of India?

Experts say the factors driving the current selloff is a mix of factors: attractive valuations in developed markets, rupee depreciation, recent US-Iran war which has driven up global crude oil prices.Pabitro Mukherjee, Associate Vice President – Technical Research Bajaj Broking blames external factors for this month’s exodus.“The current wave of FPI outflows has been primarily driven by escalating geopolitical tensions in West Asia, which have triggered a global “risk-off” sentiment. This has been further compounded by macroeconomic pressures, including a weakening Indian Rupee breaching ₹95/USD, and a sharp rise in crude oil prices, which has heightened inflation concerns and widened the current account deficit,” he told TOI.

“These factors appear largely external and cyclical in nature, linked to global uncertainty and risk aversion rather than domestic structural weaknesses,” he believes.Tanvi Kanchan, Associate Director at Anand Rathi Share and Stock Brokers Limited explains that with Brent crude prices above $100, a classic risk-off move has been fuelled. This has been compounded by the rupee hovering near ₹92-95 against the dollar, elevated US bond yields, and a mixed Q4 earnings outlook.Rising US bond yields and tightening global liquidity have improved the relative attractiveness of developed market fixed income, prompting reallocation away from emerging markets including India, she tells TOI.She is also of the view that most of these drivers are cyclical, not structural – the West Asia conflict, crude spike, and dollar strength are external shocks. “India’s domestic fundamentals, 7%+ GDP growth, fiscal consolidation, and a robust DII ecosystem, remain intact. The one structurally evolving factor is FPI reassessment of IT earnings amid AI disruption, which will take 12-18 months to play out,” she opines.What’s spooking investors is the possible economic fallout of the persistent Middle East crisis.“Approximately 70-80% of the selling is externally driven on the backs of weakness in global equity markets following the West Asia war, steady rupee depreciation, fears of declining Gulf remittances, and the impact of high crude on India’s growth and corporate earnings are all contributing to sustained FPI selling. FPIs were also sellers in other emerging markets like Taiwan and South Korea, confirming this is a global risk-off move, not an India-specific rejection,” says Tanvi Kanchan.

Also, domestically, Indian valuations continue to remain relatively elevated compared to several emerging market peers, which may still be prompting selective profit-booking and reallocation, but this is a secondary factor, not the primary driver, she adds.One pointer of structural strength is the continued faith that domestic investors are showing. “While domestic institutional investors have shown strong participation, with record buying of ₹1.28 lakh crore, their support has only partially offset the scale of FPI selling, indicating that global developments are the dominant influence in the current phase,” says Pabitro Mukherjee.For Tanvi Kanchan, the silver lining is DIIs, whose monthly SIP inflows of Rs 30,000 crore and deployable mutual fund cash of around $6 billion provide a strong floor, preventing a disorderly market collapse.

What’s The Road Ahead?

Experts are of the view that the FII selling may continue through the first half of financial year 2026-27, with a clearer trend reversal possibly emerging only in the second half. However, market analysts believe in the fundamental strength of India’s economic growth story and believe that the market remains structurally sound, with possible signs of optimism emerging once the immediate war settles down and crude oil prices come below $100 per below.“FII inflows are expected to be majorly skewed towards H2FY27 because H1 earnings will be impacted by the war scenario. Key reversal signals to watch would be crude oil dropping sustainably below $90/barrel; the rupee stabilising below ₹91-92; a ceasefire or de-escalation in West Asia; Q4FY26 earnings reaffirming growth visibility for FY27; and the US Federal Reserve resuming rate cuts,” Tanvi Kanchan says.

The persistence of foreign selling is closely tied to the continuation of global risk-off sentiment and geopolitical uncertainty. As long as these conditions remain elevated, FPI outflows are likely to continue.A reversal would likely be indicated by easing geopolitical tensions, stabilisation in crude oil prices, and improvement in currency stability, which would collectively help restore investor confidence, says Pabitro Mukherjee.So when will FIIs be back on D-Street? According to Tanvi Kanchan, going forward, the key conditions are:

- Rupee stabilisation;

- Q4 earnings delivery reaffirming stable FY27 EPS growth;

- US Fed resuming rate cuts, which would ease global liquidity and improve the relative attractiveness of emerging markets like India; and regulatory moves,

- RBI’s easing of certain FPI limits and SEBI’s expanded participation framework for IFSC-based FPIs are steps in the right direction.

- A formal US-India trade agreement, if concluded, would be the single biggest FPI re-rating catalyst in FY27.

She explains that a combination of external easing and domestic policy action is needed. “On the external side we see crude oil cooling, US yield moderation, and West Asia de-escalation. On the domestic side, February 2026 showed what works, the combination of an interim India-US trade framework reducing tariff uncertainty, the Union Budget retaining fiscal credibility with a 4.3% deficit target, and valuation comfort after earlier corrections brought Rs 22,615 crore back in a single month,” the Anand Rathi Share and Stock Brokers expert says.(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India)

: Wall Street rallies on de-escalation hopes; S&P 500 jumps over 1.6%, tech stocks lead gains")

{kind=link}