MUMBAI: Banks have asked govt to review the definition of affordable housing by revising property value and size thresholds to reflect inflation and changing requirements, as rising ticket sizes and interest costs render existing limits less relevant.“We are the market leaders in housing finance and our home loan portfolio has grown by 13.7%. Our average ticket size has also gone up. The composition of affordable housing needs to change. This is what we have told govt,” said CS Setty, chairman State Bank of India.“With the passage of time, fixed limits lose their relevance. Today, it may not be possible to purchase a house within price thresholds that qualified as affordable 10 years ago. Ideally, these limits should be indexed to real estate prices,”said Keki Mistry, chairman, HDFC Bank. “Similarly, Section 24(b) of the Income-Tax Act provides for a deduction of Rs 2 lakh on interest paid on home loans. When this limit was set in 2014, it was significant; today, it covers only a small portion of the average interest outgo,” he added.

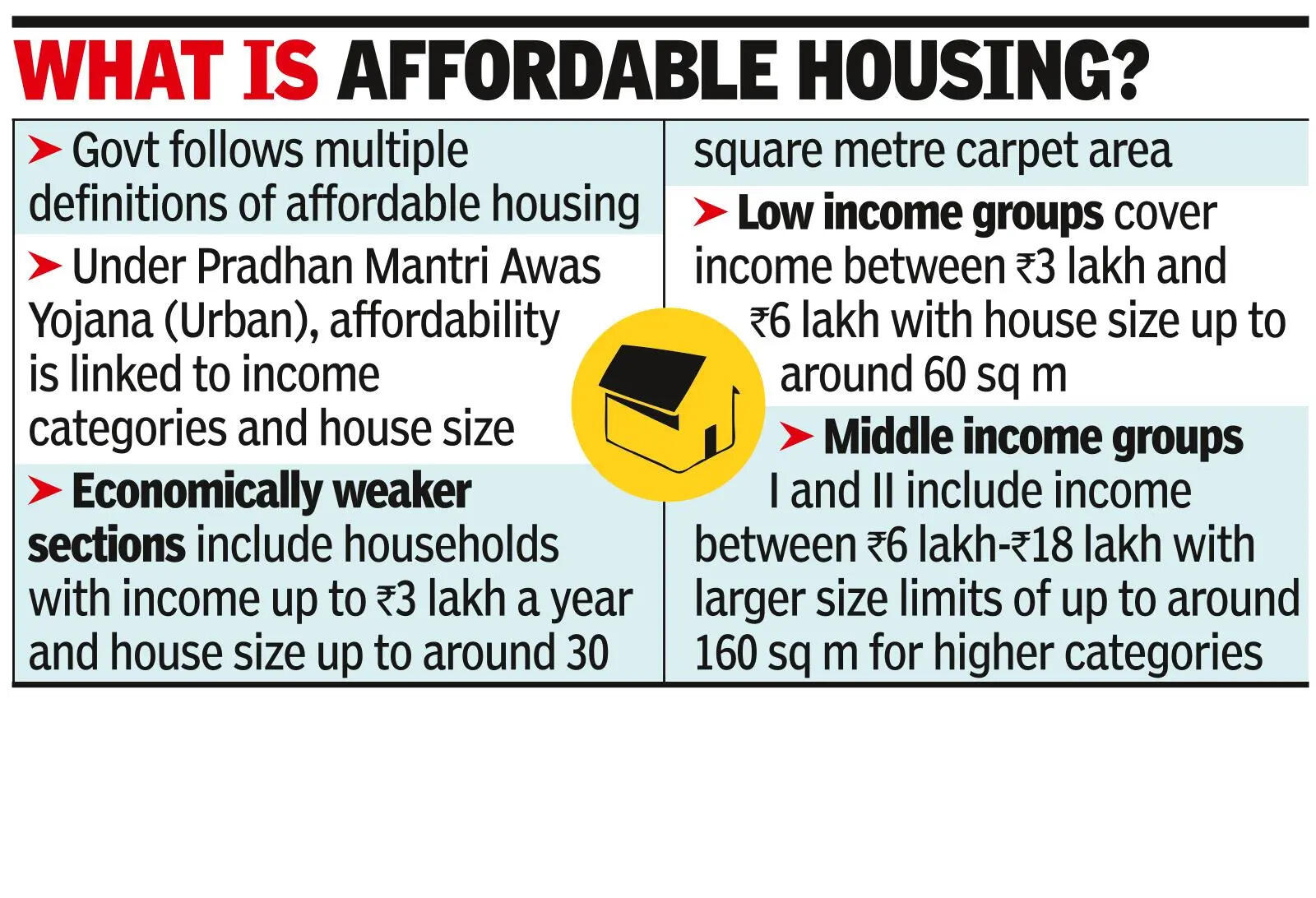

Currently, govt follows multiple definitions of affordable housing. Under Pradhan Mantri Awas Yojana (urban), affordability is linked to income categories and house size. Economically weaker sections include households with income up to Rs 3 lakh a year and house size up to around 30 sq m carpet area. Low income groups cover income between Rs 3 lakh and Rs 6 lakh with house size up to around 60 sq m. Middle income groups I and II include income between Rs 6 lakh and Rs 18 lakh with larger size limits of up to around 160 sq m for higher categories.In Jan 2026, the Confederation of Real Estate Developers’ Associations of India (Credai) called for updating affordable housing parameters. “The current definition, unchanged since 2017, restricts units to 60 sq m in metros and 90 sq m in non-metros, along with a Rs 45 lakh value cap that no longer aligns with higher land and construction costs,” the association said. The industry body said multiple definitions across schemes such as PMAY, RBI, NHB, and Rera create complexity.

{kind=link}