")

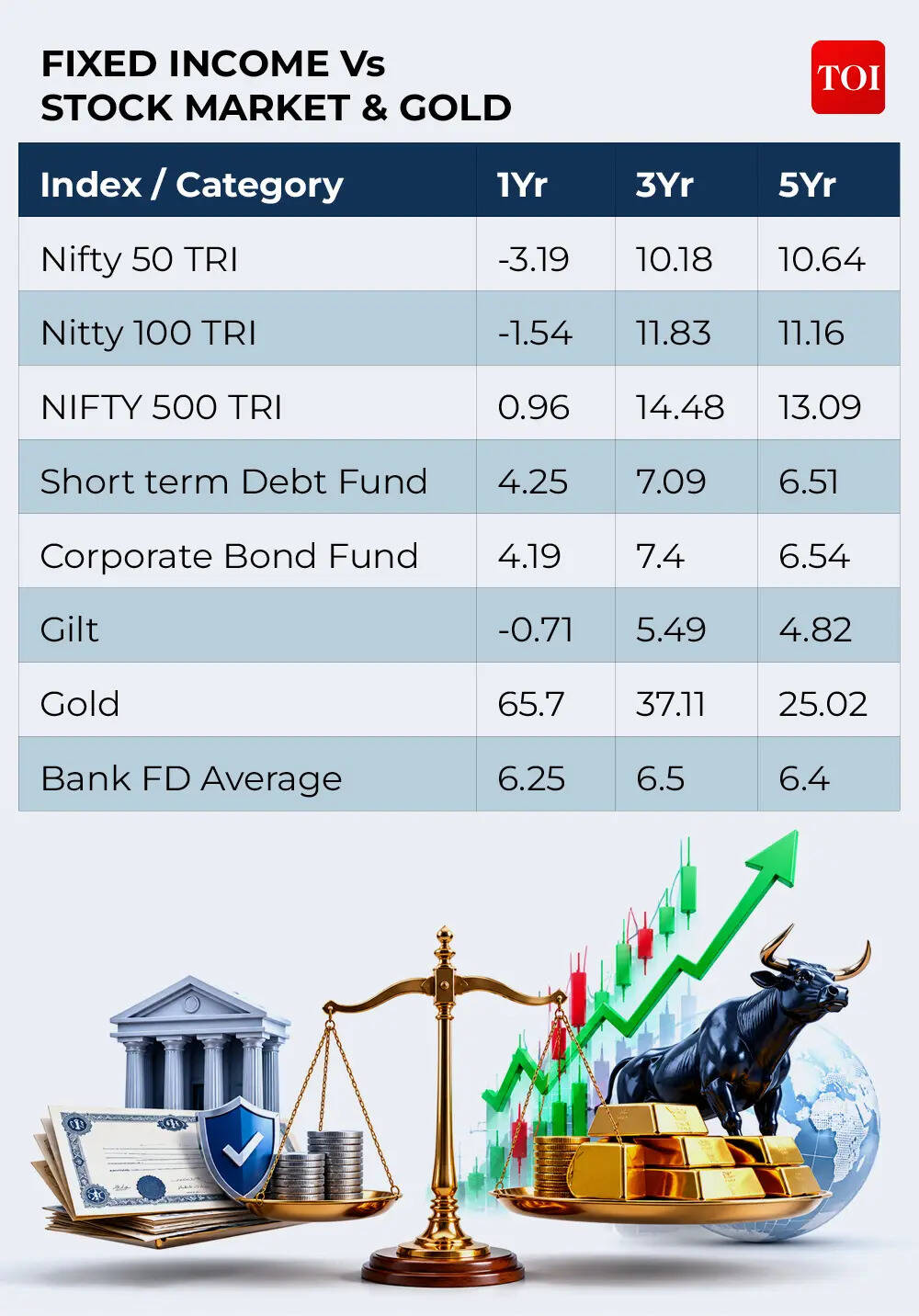

Sensex and Nifty are in deep red. Gold, the favourite safe haven asset for investors, is seeing huge volatility. The US-Iran conflict has hit investment portfolios of Indians who are now left wondering: where is their money safe? Which asset class will protect against the ongoing uncertainty & what is the ideal portfolio strategy.The age-old wisdom of ‘FD karana’ may just be your answer, but to what extent? Fixed deposits and other fixed income instruments are the quiet, but effective shield in your portfolio that may give lower returns than other asset classes, but also act as the biggest protection in times of volatility when equities tumble.Mohit Gang, Co-Founder & CEO of MoneyFront describes them as a safe harbor for investors in volatile times. He sees them as an all-weather allocation to provide safety, liquidity and stable steady returns to a portfolio.Financial Planner Rohit Shah provides an interesting perspective on how important fixed income assets are for your portfolio: Think of it like the brake in a car – you don’t use it all the time, but when you need it, nothing else works. As experts note: Every crisis reminds us that markets can swing like a pendulum between greed and fear. Fixed income offers comfort in those phases and does its job as a stabiliser. But history also shows that investors who stay parked in fixed income for too long usually lag on inflation‑adjusted returns.

Fixed Income: No One-Size-Fits All

According to Rohit Shah, for senior citizens, bank FDs work well due to higher rates and tax breaks. “Government schemes and bonds suit those seeking safety and predictable returns. Debt mutual funds help with market‑linked returns and tax efficiency over the right time frame. The choice should follow the time horizon, tax bracket and the goal the money is meant for,” he tells TOI.

Nirav Karkera, Head of Research, W by Groww says investors should not view fixed income as one homogenous category. Different products solve different problems.

- Fixed deposits remain relevant for conservative investors who want certainty, simplicity and capital protection over shorter horizons. They work well for emergency funds, near-term goals and investors who prioritise predictability over tax efficiency.

- Government bonds and gilt funds can become attractive when yields are reasonable and inflation appears to be stabilising. These are better suited for investors with a medium-term horizon who can tolerate interim mark-to-market volatility, Karkera says.

- Corporate bond funds look relatively constructive where portfolios are focused on high-quality issuers. Accrual yields are healthy and India’s corporate balance sheet environment remains reasonably strong. The emphasis, however, should remain on credit quality rather than yield maximisation, the expert says.

- Money market funds and short-duration funds are suitable for investors seeking liquidity, moderate stability and potentially better post-tax outcomes than idle balances in savings accounts.

- For investors in higher tax brackets, arbitrage funds have become increasingly relevant. They offer relatively low volatility and benefit from equity taxation, making them useful for parking money where the investment horizon and risk profile are appropriate.

- Small savings schemes continue to appeal to conservative households because of sovereign backing, stable rates and familiarity. They are particularly useful for retirement-oriented or income-focused investors.

“The broader fixed income strategy today should be to focus on quality accrual, maintain liquidity and stagger duration exposure. Investors do not need to take aggressive long-duration calls unless their horizon and risk tolerance justify it,” Karkera says.

Fixed income: Factors you shouldn’t miss

The common takeaway after talking to experts is clear: while fixed income can shield you in times of volatility, its long‑term record of beating inflation is poor. Hence, financial experts advocate for a balanced portfolio.“If you lean too much on fixed income, purchasing power may quietly erode. Just like a balanced meal needs carbs, protein, healthy fats, vitamins, minerals and water, a balanced portfolio needs equity, fixed income and other assets in the right mix, based on goals and risk appetite,” says Rohit Shah.Nirav Karkera, Head of Research, W by Groww explains that each fixed income asset carries a different combination of credit risk, liquidity risk, duration risk, reinvestment risk and tax impact. The yield offered by the product is essentially compensation for one or more of these risks.A high-quality short-duration product behaves very differently from a long-duration gilt fund or a lower-rated corporate bond strategy. The former is designed for stability and liquidity. The latter may offer higher return potential, but can also see sharper price movements when interest rates change.

Inflation is another important limitation, he says. Most fixed income instruments do not automatically protect purchasing power. If inflation rises and interest rates move up, longer-duration fixed income products can see price declines. This is basic bond mathematics. Higher yields generally mean lower prices for existing bonds, especially those with longer maturity profiles.Karkera points out that taxation also matters. A product may look attractive on a pre-tax basis but deliver a much weaker outcome after tax. Investors should therefore evaluate fixed income on a net return, risk-adjusted and time-horizon basis.In short, fixed income can protect portfolios from excessive volatility, but it is not a universal shield against inflation, taxation or poor product selection, he says.

What should your portfolio strategy be?

History shows that during periods of market stress, high-quality fixed income usually plays the role it is designed to play; it absorbs shocks, preserves liquidity and gives portfolios a steadier foundation.“During episodes such as the 2013 taper tantrum, the 2018 oil shock and the 2022 global inflation and Ukraine crisis, equities saw significant volatility. In contrast, quality fixed income instruments generally offered better stability and more predictable outcomes, especially for investors who avoided excessive credit or duration risk,” says Nirav Karkera.The key lesson is that quality matters. Fixed income is defensive only when the underlying portfolio is built with discipline. Chasing yield blindly can convert a supposed safety allocation into a hidden risk allocation, he adds.

So, in the current scenario, what should investors do to protect their wealth? According to Rohit Shah, the key is to revisit, not reinvent, your asset allocation. Check if equity, debt and gold weights have drifted too much from your plan, and rebalance where required. The strategic allocation usually doesn’t need a complete overhaul. Keeping some dry powder in safer assets also lets you deploy calmly when others are forced sellers, he says.During times of crisis and war, money does move into safer assets and fixed income gets attractive. But this time around, the crisis is resulting in soaring inflation, which in turn is spiking the yields across tenors and geographies. “For existing investors, this could mean some mark-to-market losses but for newer investors this could be an opportune time to lock yields at higher levels. Hence, fixed maturity or target maturity products could find favour once the yields go further up,” Mohit Gang recommends.Ultimately, your asset allocation should be a factor of your liquidity preferences, time horizon and risk tolerance. Experts recommend a fair mix of all assets viz: risk assets like equities, fixed income and commodities to have a robust all-season portfolio. “Equities should remain the core allocation for long-term wealth creation. Fixed income should provide stability, liquidity and visibility for short- to medium-term goals. Gold can continue to serve as a portfolio diversifier, but investors must recognise that gold is not volatility-free. It can protect portfolios in certain macro environments, but it can also move sharply in both directions over shorter periods,” says Nirav Karkera.The bottom line is: Fixed income instruments can offer stability especially during periods when stocks and equities are falling and gold or silver remain volatile. But experts say that investors should avoid shifting money within their portfolio purely driven by panic. Unlike equities, which are meant for long-term wealth creation, fixed income products are designed to provide predictable returns, capital protection, liquidity and income stability over defined time horizons. They can also help reduce overall portfolio volatility during turbulent market phases. However, the ideal allocation should depend on the purpose of investment rather than short-term market movements. As Nirav Karkera sums up: The crux remains that volatility should not force investors into reactive decisions. It should push them back to discipline, asset allocation and product suitability.(Disclaimer: Recommendations and views on the stock market, other asset classes or personal finance management tips given by experts are their own. These opinions do not represent the views of The Times of India.)

{kind=link}